Do you want to know about ULIP and how it is different from mutual funds? Well, let’s get back into the past when there was a time when stocks were used to manually exchanged under a banyan tree in Mumbai. We have come way far since then.

Today, there are plenty of financial product options available to investors all around the globe to invest their hard-earned money for some return.

Depending upon your financial goals, needs, and limitations, you can opt for any of these options either to safeguard your wealth or to create more, or to get insured.

What are Mutual Funds and ULIP?

Mutual Funds are a very common investment option available to investors today. In simple words, it’s more like an investment vehicle that accumulates money from the investors and then invests that money on behalf of the investors in different assets to get some return. It’s more like a bus you take, the driver takes the passenger to a single destination. Here, the driver is the fund manager, the bus is referred to a mutual fund scheme and the passenger denotes to be an investor.

Mutual fund term is often interchanged with another financial product knowns as ULIP (Unit-Linked Insurance Plans). These are insurance policies serving the dual purpose of insurance cover as well as earns you a return by investing. The insurance companies also float funds to gather money from investors just like mutual funds. Then it invests your money in different assets like stocks and bonds. Sounds like a mutual fund, right? But they are not alike.

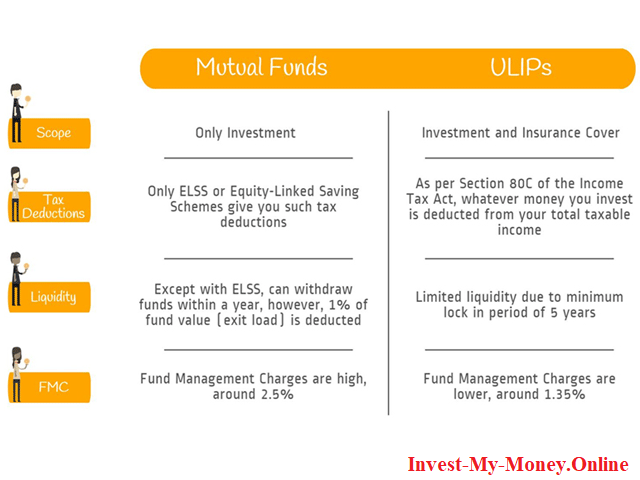

What is the Difference Between Mutual Funds & ULIP?

The main difference lies in mutual funds is that it doesn’t cover life insurance, whereas ULIPs do. This is the money company promises to give to an investor’s family in case of an untimely death.

Let us understand this by taking an example:

Mr. X invests 50,000 in a ULIP, while Mr. Y invests the same amount in mutual funds. However, a part of Mr. X’s investment is taken as insurance cover every month, which acts as an “insurance premium” or “protection element“. This buys Mr. X an insurance cover of 5 lacs. Whereas, Mr. Y needs to buy him a separate insurance policy for life cover. Now, in the case Mr. X meets any accident and passes away, then the family of Mr. X is eligible for getting the compensation of 5 lacs or the funds value, whichever is higher. This will not be the same for Mr. Y.

Table of Contents